What Does Kam Financial & Realty, Inc. Mean?

Wiki Article

Everything about Kam Financial & Realty, Inc.

Table of ContentsAll About Kam Financial & Realty, Inc.Kam Financial & Realty, Inc. for BeginnersThe smart Trick of Kam Financial & Realty, Inc. That Nobody is DiscussingSee This Report on Kam Financial & Realty, Inc.Kam Financial & Realty, Inc. Fundamentals ExplainedThe Ultimate Guide To Kam Financial & Realty, Inc.

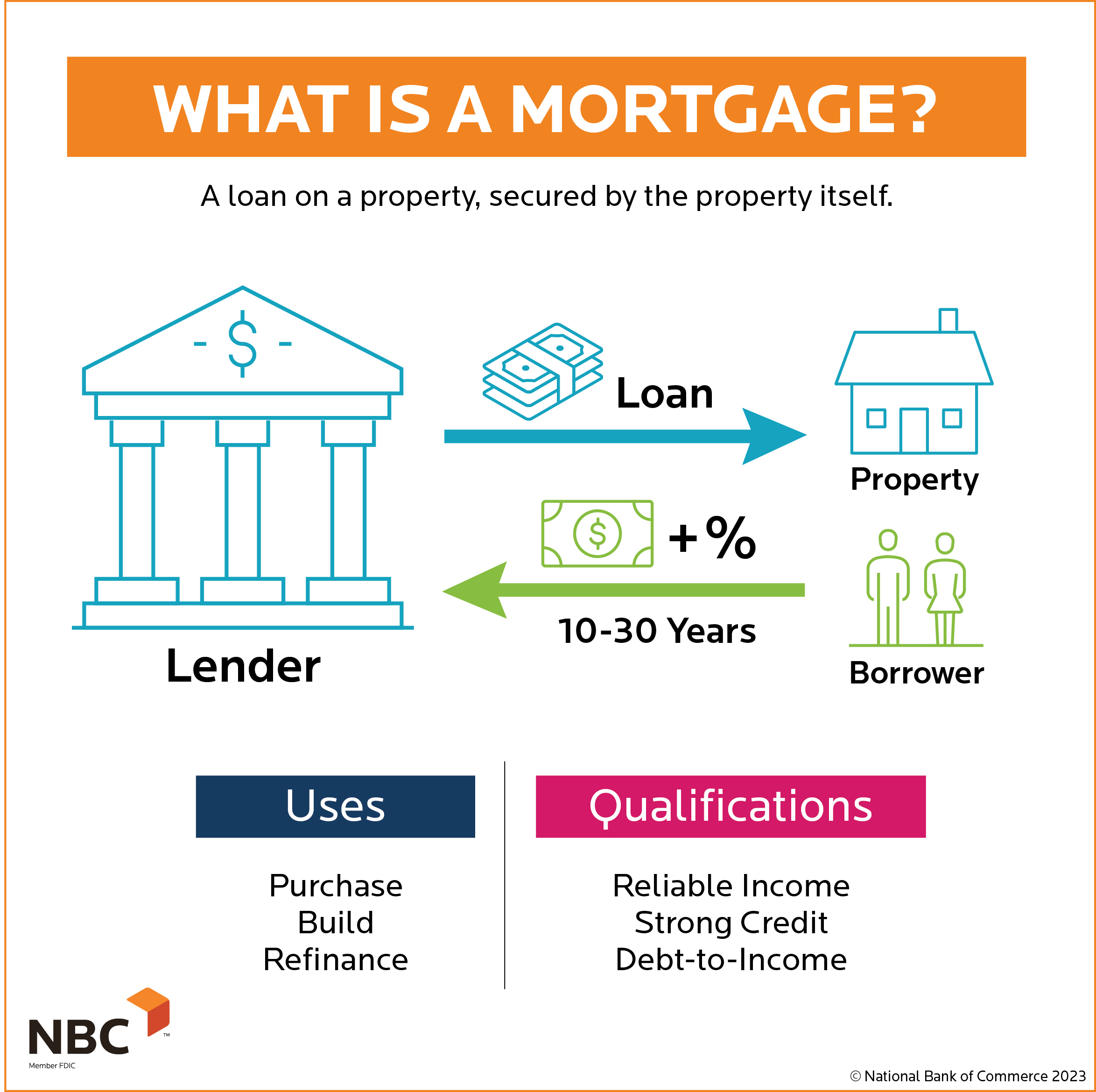

A home loan is a funding used to acquire or maintain a home, plot of land, or other realty. The customer agrees to pay the lender over time, usually in a collection of routine payments split right into principal and interest. The home then works as collateral to protect the finance.Home loan applications undergo a strenuous underwriting procedure before they get to the closing phase. The residential property itself serves as collateral for the finance.

The price of a home mortgage will certainly depend on the kind of car loan, the term (such as thirty years), and the rates of interest that the lending institution fees. Home mortgage rates can differ widely relying on the kind of product and the qualifications of the applicant. Zoe Hansen/ Investopedia People and businesses utilize mortgages to buy property without paying the whole acquisition price upfront.

Things about Kam Financial & Realty, Inc.

The majority of traditional home mortgages are completely amortized. Typical home mortgage terms are for 15 or 30 years.

A residential buyer promises their home to their lending institution, which then has an insurance claim on the property. In the case of foreclosure, the lending institution might evict the citizens, offer the residential or commercial property, and utilize the money from the sale to pay off the home mortgage debt.

The lender will request evidence that the debtor can repaying the lending. This might include bank and financial investment declarations, current tax returns, and proof of current employment. The lender will typically run a credit check as well. If the application is approved, the lender will offer the borrower a car loan of as much as a certain quantity and at a specific rates of interest.

How Kam Financial & Realty, Inc. can Save You Time, Stress, and Money.

Being pre-approved for a home mortgage can offer buyers a side in a limited real estate market since sellers will understand that they have the cash to back up their deal. When a customer and seller concur on the regards to their offer, they or their agents will certainly satisfy at what's called a closing.The seller will certainly move possession of the property to the buyer and obtain the agreed-upon sum of money, and the customer will authorize any continuing to be home loan records. There are hundreds of options on where you can obtain a mortgage.

10 Simple Techniques For Kam Financial & Realty, Inc.

The common sort of mortgage is fixed-rate. With a fixed-rate home loan, the rate of interest remains the exact same for the whole regard to the lending, as do the customer's monthly settlements towards the home loan. A fixed-rate home loan is also called a conventional home loan. With an adjustable-rate mortgage (ARM), the rate of interest is dealt with for an initial term, after which it can change periodically based upon dominating interest rates.

6 Easy Facts About Kam Financial & Realty, Inc. Described

The entire car loan equilibrium comes to be due when the debtor passes away, moves away permanently, or sells the home. Factors are essentially a fee that borrowers pay up front to have a lower interest rate over the life of their car loan.

Not known Facts About Kam Financial & Realty, Inc.

How much you'll have to spend for a home mortgage depends on the type (such as fixed or flexible), its term (such as 20 or 30 years), any type of discount rate factors paid, and the rates of interest at the time. california loan officer. Passion rates can vary from week to week and from loan provider to loan provider, so it pays to look around

If you default and confiscate on your mortgage, nevertheless, the financial institution might end up being the brand-new proprietor of your home. The cost of a home is often far more than the amount of cash that the majority of families save. Consequently, home mortgages enable people and family members to buy a home by taking down only a relatively tiny deposit, such as 20% of the her explanation purchase price, and getting a financing for the balance.

Report this wiki page